Quick summary

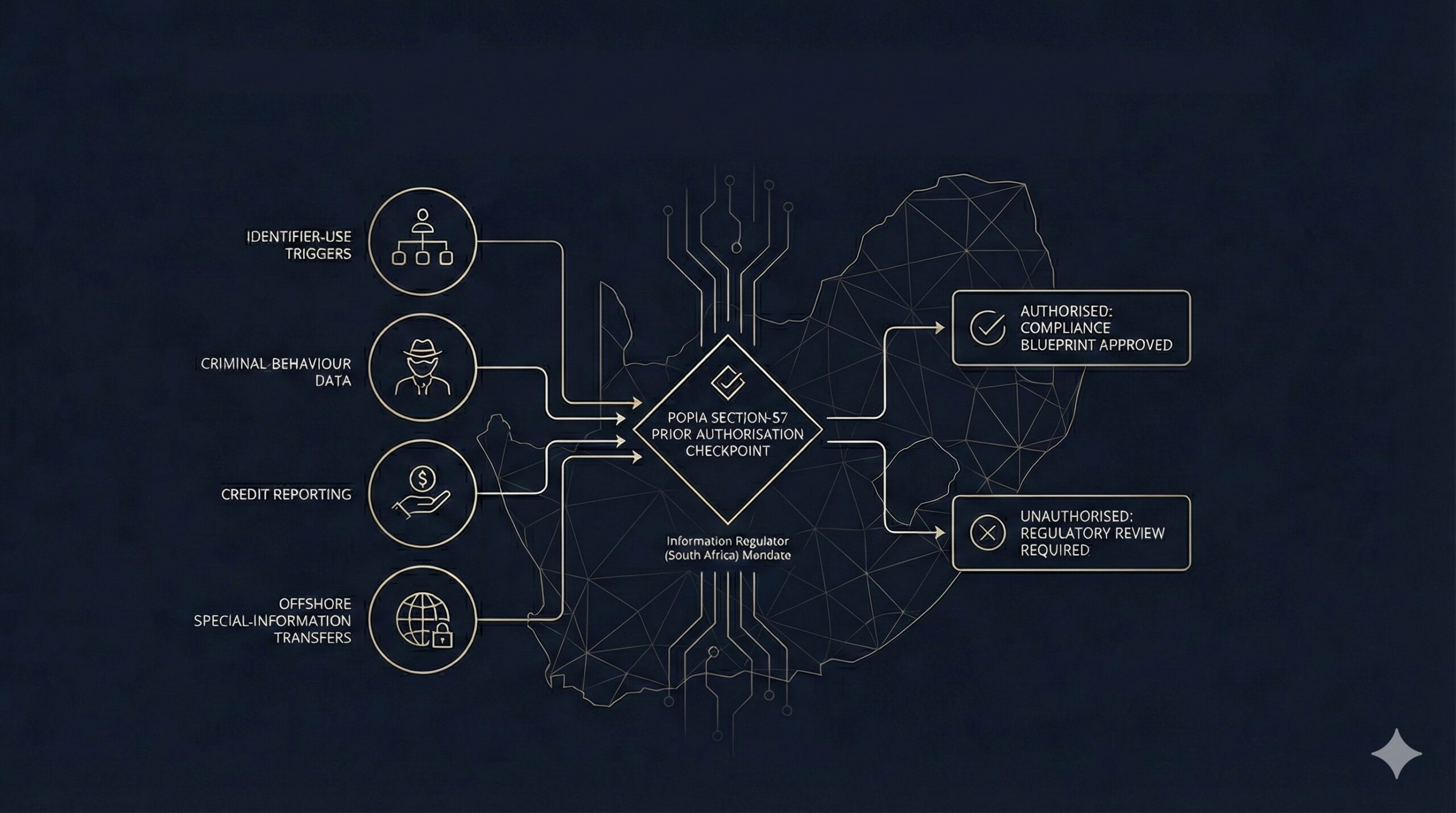

POPIA requires prior authorisation from the Information Regulator before organisations process personal information in four high-risk categories:

- re-purposing unique identifiers together with data from other responsible parties;

- processing information about criminal or unlawful conduct;

- credit reporting or behavioural credit profiling; and

- offshore transfers of special personal information or children’s data to jurisdictions without adequate protection.

If any of these triggers apply, processing must not begin until the Regulator grants authorisation or confirms that no detailed investigation will be conducted. The application process effectively serves as a compliance audit, requiring evidence of full alignment with POPIA’s lawful-processing conditions, governance measures, security safeguards, and subject-rights enablement.

Only narrow exemptions exist: notably where an approved POPIA Code of Conduct covers the processing, or where prior authorisation has already been granted and the processing purpose remains unchanged.

In short: if your operations involve identifier-matching, external data enrichment, criminal-behaviour analysis, affordability or risk-banding engines, or cross-border transfers of sensitive data, you must assess whether section 57 is triggered before processing begins.

Context

South Africa’s Protection of Personal Information Act (POPIA) creates a powerful supervisory mechanism for certain high-risk processing activities: prior authorisation. Where section 57 applies, the responsible party must stop processing until the Information Regulator investigates, assesses compliance, and grants approval.

In a time of identity-layer data, behavioural analysis, digital-mobility ecosystems, finance scoring, telematics, and AI-powered risk models, prior authorisation has shifted from obscure legal chapter to executive-level compliance priority.

This page explains:

- when prior authorisation is mandatory,

- how the process works,

- how the Regulator evaluates applicants, and

- strategic readiness indicators for organisations.

It is written for compliance leaders, CIOs, CROs, CISOs, information officers, legal counsel, and data-governance decision-makers in South Africa and the broader EMEA market.

When POPIA requires prior authorisation

A responsible party must obtain authorisation before processing begins if it intends to engage in any of the following categories:

Use of unique identifiers for new or linked purposes

Where an identifier, such as:

- identity number,

- bank-account number,

- student or employee number,

- phone number,

- policy number,

will be used for a different purpose than originally collected, and with the aim of linking it to information processed by other parties.

Typical environments include:

- data-enrichment programmes,

- customer-360 mapping,

- fleet-identity consolidation,

- shared-services data lakes,

- telematics-driven risk scoring,

- mobility-finance eligibility models.

Processing information relating to criminal behaviour

This includes data relating to:

- criminal conduct,

- unlawful acts, or

- objectionable behaviour,

especially when processed on behalf of third parties.

Recruitment vetting, insurers, investigative-risk services and integrity-screening tools frequently cross this threshold.

Processing for credit reporting

Where the processing is linked to credit reporting or credit-behaviour profiling, prior authorisation applies.

This is especially relevant for:

- finance houses,

- credit bureaus,

- mobility-finance engines,

- credit-worthiness classifiers,

- affordability-decision platforms.

Offshore transfer of special personal information or children’s data

If special personal information (such as biometrics, health data, religious or political affiliations) or children’s data is transferred to a foreign country that lacks adequate data-protection safeguards, authorisation is mandatory.

This affects:

- cloud-hosted environments,

- cross-border SaaS platforms,

- offshore service-desk teams,

- global-group IT architecture,

- analytics platforms with foreign nodes.

See the Regulator’s form for authorisation to process special personal information.

Consequences of non-compliance

- criminal offences,

- enforcement notices,

- forced redesign of systems and architecture,

- regulatory sanction,

- litigation risk,

- reputational loss.

Prior authorisation must therefore be actively built into governance planning for all high-risk processing categories.

Exemptions from prior authorisation under POPIA

POPIA recognises a limited set of circumstances in which the prior-authorisation requirement under section 57 does not apply. These exemptions are narrow, and organisations should only rely on them where the statutory conditions are clearly satisfied.

- Approved Codes of Conduct: Where a sectoral Code of Conduct has been issued by the Information Regulator and brought into force under Chapter 7, sections 57 and 58 do not apply. In those cases, the obligations, controls and safeguards contained in the Code take precedence over the prior-authorisation regime.

- Once-off authorisation (unless processing changes): If a responsible party has already received prior authorisation for the contemplated processing, a repeat application is not required, provided that the purpose, scope, method and risk profile of the processing remain consistent with the conditions for which authorisation was granted. Any material departure may trigger a fresh application.

- Unique identifiers used strictly for original purpose: Section 57(1)(a) is only triggered where a unique identifier is used for a new purpose and linked with information processed by another responsible party. Where identifiers are processed solely for their original collection purpose—and are not combined, matched or repurposed—the prior-authorisation obligation falls away.

No other exemptions apply

Routine arguments such as commercial necessity, contractual mandate, research justification, internal investigations, or operational expediency are not recognised exemptions. If the processing fits within any of the listed Section 57 triggers, prior authorisation remains mandatory unless one of the narrow exemptions above applies.

Regulator extension of trigger categories

Section 57(2) empowers the Regulator to expand the scope where processing may pose a particular risk to the legitimate interests of data subjects.

Likely emerging categories include:

- algorithmic behavioural scoring,

- biometric authentication ecosystems,

- mobility patterning,

- federated digital ID,

- model-training datasets involving personal information,

- large-scale identity aggregation networks.

Processing must stop until approval is granted

Once section 57 is triggered:

- the Regulator must be notified; and

- processing must be suspended until clearance.

Proceeding without authorisation is unlawful and may constitute a statutory offence.

What the Regulator evaluates

Prior authorisation is not a box-ticking exercise: it is a mini compliance audit. The Regulator expects evidence that all eight POPIA conditions for lawful processing are met:

Accountability

Governance frameworks, policy instruments, oversight processes, records-of-processing, and compliance operating models.

Processing limitation

Data minimisation, lawful basis, necessity, justification, direct collection, and appropriate consent architecture (where applicable).

Purpose specification

Lawful, explicit, legitimate purpose directly tied to a business function or organisational activity.

Further processing limitation

Compatibility testing of secondary processing with the original purpose.

Information quality

Accuracy controls, update processes, data-lifecycle mapping, retention rules, and verification processes.

Openness

Transparency notices, PAIA disclosures, documentation of processing, internal audit trails.

Security safeguards

Technical and organisational controls: encryption, access control, audit logs, resilience, intrusion detection, and breach-response capability.

Data-subject participation

Mechanisms for:

- access,

- correction,

- deletion,

- objection, and

- revocation of consent.

If these cannot be proven, authorisation is unlikely.

How the prior-authorisation process works

Step 1: Internal trigger assessment

Conduct an internal legal and data-mapping review to determine whether section 57 applies.

Step 2: Formal notification

Notify the Information Regulator of the intended processing.

Step 3: Comprehensive application submission

The Regulator requires an evidential dossier demonstrating:

- legal basis,

- POPIA-condition compliance,

- safeguarding and governance maturity,

- justification of necessity,

- identifier logic,

- foreign-jurisdiction adequacy analytics.

Step 4: Initial review

The Regulator confirms whether a detailed investigation is required.

Step 5: Processing suspension

Suspension remains in force until the Regulator issues an outcome.

Step 6: Final determination

The Regulator issues a statement confirming lawfulness or triggering enforcement mechanisms.

Step 7: Deemed authorisation

If timelines expire and the responsible party has fully complied with notification requirements, authorisation may be presumed.

Emerging exposure areas ITLawCo monitors for clients

- AI-powered risk engines

- Driver-behaviour models

- Fleet telematics

- Vehicle-identity mapping

- Federated authentication systems

- Student-funding eligibility analysis

- Cross-border cloud stack hosting

- Recruitment and misconduct vetting

- Combined identity and scoring models

For many organisations, Section 57 is not theoretical; it is already operationally triggered.